The Stock Market

A brief look at this investment class

We’re in the money, we’re in the money.

We’ve got a lot of what it takes to get along.

We’re in the money, the skies are sunny.

Old man Depression, you are through, you’ve done us wrong.

We never see a headline about a breadline today.

And when we see the landlord, we can look that guy right in the eye.

We’re in the money, come on, my honey,

Let’s spend it, lend it, send it rolling along.

- We’re In The Money, Gold Diggers of 1933 (musical), Al Dubin and Harry Warren

- The Wall Street Experience")

Though there are a great number of investment options out there, you’ll find that in general conventional savings performs relatively anemically, bonds tend to be somewhere around breakeven net of inflation (with certain exceptions for high yield “junk” bonds famously available from time to time and also infamously burning their investors every now and again), commodities (counterintuitively, despite the name) being potentially more volatile, and as a very broad rule of thumb: the stock market - fractional equity ownership - has been the growth engine of wealth in a vastly disproportionate manner. Now, there’s a time and a place for everything - and many people find some level of comfort in a portfolio of tax-free municipal bonds - but that otherwise fine example is one typifying a choice inevitably purchased as a stable income play and not something to grow your wealth, so I’m going to set it aside. I’m also not going to talk about cryptocurrencies today - or commodities, real estate, energy, or the foreign exchange market - though I might revisit those later.

One might also immediately ask: hey wait, wise guy, how about exotic asset classes or investment strategies like hedge funds - we expected you to at least touch on those? Well, ok, here’s the overview: at least in theory, hedge funds should be in a position to make money whichever way the market goes (up or down) and that equally importantly they de-risk against the market going the wrong way - a process called hedging, from which the name is derived. In practice, many hedge funds do that, or at least aspire to, but are more or less leverage funds - a term which means they basically rely on the ability to borrow a multiple of the money they control and make particularly disproportionate investments when they see a market opportunity, in order to generate an outsized return. But also… due to the regulations around this space (and the perceived risks and complexity), they are typically limited to accredited investors or institutions, which you should read as “you have to be rich”. (It’s actually not that hard to come by: a net worth over a million dollars excluding your primary residence or an income over $200,000 a year will qualify you, or a handful of other means - here’s the SEC link.) But still, it’s unlikely that most people can readily invest in a hedge fund - I’ll talk more about this later, but for the moment, let me come back to it and resume talking about the core stock market.

For what it’s worth, Warren Buffett’s advice to someone who did not want to spend a great deal of time studying the market was to invest 90% into the S&P 500 (through an index fund - he recommended a low-cost one like Vanguard) and 10% into short term government bonds. And let’s be fair, he’s pretty much up on a pedestal as the investor who does it right.

So let’s start by taking a look at that recommendation. (If you want to skip the rest of this article: it’s a pretty good call; you can basically make a small contribution out of every paycheck into exactly this strategy, ideally at least partially in your IRA to defer against taxes for long term growth - and probably some portion outside the IRA because you’ll want some liquidity from time to time - but if you want an investment thesis that fits on a business card, buy into a solid index fund a little bit every paycheck and try to just let it grow long term.)

The stock market lets you buy shares (small equity ownership pieces) in companies. When those companies grow and become more valuable, your shares can increase in price, and many pay dividends (cash distributions to shareholders). Over time, this can compound dramatically through reinvestment.

The Standard and Poor’s 500 Index is a basket of stocks - a stock market index - that tracks the performance - as you might have guessed - 500 of the largest publicly traded companies in the United States. It is widely considered a "barometer" for the overall health of the U.S. economy and stock market because it covers roughly 80% of the total U.S. equity market capitalization. The S&P 500 is very durable and has grown well over the years - the stocks that make up this index get swapped out fairly frequently as the market evolves and changes, and companies merge and are acquired.

This index uses a float-adjusted market capitalization weighting, meaning larger companies have a significantly greater impact on the index's value than smaller ones. This becomes especially obvious when you look at how the overall distribution of the index breaks down - it’s not split evenly across all five hundred stocks. While it contains 500 companies, the top 10 stocks - currently including Nvidia, Alphabet, Apple, Microsoft, Amazon, Broadcom, Meta, Tesla, Berkshire Hathaway, and Eli Lilly - account for approximately 38% of the index's total value. (The top 50 stocks account for 60% of the whole index, leaving the other 450 to make up the other 40%.) In order to be included in the S&P 500 index, stocks are selected by a committee based on several factors, including a minimum market cap of $22.7 billion (as of early 2026), high liquidity, and positive earnings over the four most recent quarters.

Now as a very broad rule, investing in the stock market is one of the most effective ways for individuals to build long-term wealth, as stocks have historically delivered average annual returns of around 7–10% after inflation over long periods (though as will always be said, past performance doesn’t guarantee future results).

Mostly people will invest in stocks to beat inflation - after all, cash in savings accounts usually loses purchasing power over decades, and bonds tend to do better but still don’t generally much outperform inflation. Certainly, any long-term investment strategy relies on what’s termed compound growth (you’ve probably heard this term as “compound interest”, but it’s applicable in equities as well) - basically, the premise is that superior returns generate more returns (and that this is especially powerful over a long horizon of a decade or several… if you have 30 years of compounding, it really adds up). Also, stocks tend to be very accessible today: in 2026, you can start with very small amounts thanks to fractional shares and low or commission-free trading on many platforms.

But let’s be clear - the general trend of “the stock markets tend to go up” is a very loose trend - they bounce around an awful lot, and depending on when you bought in, you might be waiting years and years to get back to the price you bought in at if you happened to buy “at the top of the market” just before things melted down. Because market crashes are infamously a thing - and even on a smaller scale, drawdowns regularly happen. The general term for this is volatility - when someone tells you that stocks (or other markets) are volatile, that basically just means they can fluctuate a fair bit: prices can drop 20–50% in bad years (or worse during recessions), so they’re best for money you won’t need for at least 5–10 years.

The S&P 500's maximum historical drawdown (peak-to-trough decline) is approximately 86%, occurring during the Great Depression. In modern history, major drawdowns include the 2000-2002 dot-com bust (-49%) and the 2008 financial crisis (-56%). Annual, intra-year drawdowns average roughly 14%. The most recent significant decline in 2022 was 25.4%, but the COVID-19 crash in 2020 was about 34% (though that one recovered the same year thanks to some “helicopter drop” stimulus… that sent shock waves of inflation through the economy, but to be fair letting it go unmitigated would have been worse). As of early 2026, the market remains robust near all-time highs.

This doesn’t mean that all stocks were hit equally, of course. Pets.com was obliterated during the dot-com crash (so was Webvan, which looked more based-in-reality than “we’ll FedEx you a 25 pound bag of dog food and we’ll cover the shipping”). Amazon got clobbered down to eight dollars a share during the dot-com crash - just imagine if you’d had the foresight to buy then, huh? (But people still like to misquote a premature forecast of death “Amazon dot toast” from 1998.) Actually, if you want to pick an even better buying opportunity, you could have bought right after 9/11, I believe, when it was briefly below six bucks a share. Took almost a decade to get back to where it had been in 1999 - and after that, look out world.

It might be a little unnerving to realize that most of us probably were impacted by three of the “big ones” as far as S&P 500 market crashes (dot-com crash + 9/11 followon, the Great Recession, and the COVID-19 crash) - either directly or tangentially - and we may not exactly be out of the woods yet; do we have another AI tech bubble underway and possible crash ahead? I shall avoid going off on this side discussion for the moment, but an increasingly financialized world looks a little bit precarious and it’s less clear who might bail out a meltdown of an increasingly nationalistic and decoupling system if the economic great power struggle starts to look make the global economy look dyspeptic.

(Alternately, if you want to squint at these and call them longer term trends: 1929-1939 was the Great Depression, the 1970s was the Lost Decade of Stagflation largely due to OPEC, and the 2000s started with the dot-com crash and 9/11, sputtered along for a bit during the GWOT, and then hit the 2008 economic crash so 2000-2009 ended up pretty rough also.)

What you might in general want to keep in mind is that your investment thesis is generally better made for the long term. (This is predicated on a long term investment strategy, of course, which is what everyone including me is going to tell you to do - I know it looks like you can theoretically pick stocks, watch them rise and sell them in just a few hours, days, weeks or months - a practice called day trading - but in practice, mostly this is not something to do casually, and you may tend to get fooled by luck into thinking you are skilled at it.) While drawdowns are severe, the market historically recovers, with the COVID-19 crash seeing a particularly fast rebound - basically in the same year, due mostly to the stimulus funds juicing the economy. Keep in mind also that you’re likely to see intra-year volatility: even in years with positive total returns, the market often experiences double-digit drops. Lastly - and this can be the hardest for any of us to learn or put up with: patience… recovering to previous peak levels (breaking even) can take several years, with a median of 2.5 years for stocks that do recover. This is one important reason Buffett advises you to step into index funds - it separates you from watching individual stocks rise and fall, and second-guessing them or attempting to time them. It’s also really easy to dollar-cost-average in every month out of your paycheck, for instance.

Consistently timing the market - accurately buying at the absolute lowest point and selling at the highest - is for all practical purposes impossible for most investors, as it requires predicting short-term market movements correctly twice (entering and exiting)

Research shows that staying invested over time generally beats trying to time the market, as missing just a few top-performing days can significantly reduce returns.

While some traders make use of various technical analysis tools to identify and catch market trends - (I won’t go into those today, but let me know if you want an article overviewing technical analysis in the future) - historical evidence certainly indicates that “time in the market” is a much safer and more effective strategy for long-term wealth creation. Remind yourself: if it was easy, everyone would do it. Then look at Jim Cramer. There is a famous trading strategy called the Inverse Cramer which basically takes the opposite of every trade the dude recommends on Mad Money or his other public channels - for a while this substantially outperformed the market, which gives you an idea of just how bad the supposedly professional recommendations of Jim Cramer were doing. Ultimately this is mostly a matter of how much effort you are willing to invest in trying to understand the market and produce outsized returns.

| Never Felt Better")

In the interest of full disclosure, I will point out that there was a very successful trading strategy that did its best to follow the trades of Speaker of the House Nancy Pelosi, who famously had made an absolute fortune in the stock market with her … let’s say, unique insight into how Congress might impact certain company’s future prospects. Wall Street Bets turned this into an ETF, given her amazing investment performance. It outperformed even the Inverse Kramer. (There are many reasons this was not going to actually work as an actual trading strategy, not the least of which is that Congress doesn’t have to report trades for several days after they make them, but it still did very well.)

What it comes down to is that for the vast majority of people… yeah, including most professionals… consistently timing the market is not realistic or successful over the long term.The overwhelming body of evidence from decades of studies, simulations, and real-world performance data shows that attempts to predict market highs and lows usually don’t work out (or even backfire). Investor wags like to use the phrase: “time in the market beats timing the market.” That probably sounds wrong, but let me see if I can convince you.

It costs you a lot of time, effort, attention, and transaction costs - generally including things like taxes paid (and sometimes commissions), but also the subtler costs of missed opportunities for the time you could have spent doing other things - to shepherd your trades all the time. Being a day trader often eats all your time - and stresses you out with second-guessing and market monitoring.

Prediction accuracy required is unrealistically high. Classic work by William Sharpe (back in 1975) showed you’d need to be correct at least 74% of the time just to match a passive index fund after costs and risks - and that’s far beyond what most evidence shows is achievable. Worse yet, you need to not only know when to sell before a crash but when to buy back afterwards (at the trough) so it’s exceedingly difficult to get this right, or really even approximately correct. In many cases, you can’t rely on getting out at the bottom either - during The Big Short, a lot of the bright people (such as our resident Cassandra Unchained Michael Burry) who knew the market was coming crashing down had to basically take their money and run, selling back the credit default swaps for a large profit because they weren’t entirely sure the banks who had written the CDSes as insurance were going to be solvent to deliver on them otherwise.

Missing the best days destroys returns. The stock market’s biggest gains often come in short, unpredictable bursts (often during recoveries). Studies consistently show that missing just the 10–20 best days over decades can cut returns by 50% or more - or even turn positive long-term results negative. For example, data on the S&P 500 shows that staying fully invested through cycles far outperforms trying to dodge downturns - especially since you’ll generally get chewed up by taxes getting in and out of the market.

But if that doesn’t convince you, then this one might stand you on your head: even “perfect” timing barely beats investing immediately. Charles Schwab’s ongoing research (updated through recent periods) compares hypothetical investors, and this is somewhat amusing to contemplate the three ends of the spectrum. First is the totally blessed Chad who always gets it right - the Perfect timer (always buys at the absolute low each year) gives the best outcome, which is of course what you would expect. More typically, you have the Immediate (or Steady) investor (who buys right away or dollar-cost averages weekly) turns out a pretty close second (the Schwab research shows it capturing 92% of perfect timing’s benefit, which is a lot better than most of us thought it would have been). But even the Cursed timer (the poor SOB who buys at the worst moment each year) still beats someone who stays in cash waiting for the “perfect” entry. The moral of this story: the cost of waiting (missing compounding) usually outweighs any timing edge—even assuming near-perfect skill - and I say usually, because there’s always some market meltdown scenario to prove me wrong where the the best possible move is to hide your money under your mattress. But there has only been one Great Depression and one Great Recession (or whatever phrase you care to use for the 2008 financial meltdown) - even the double whammy of the dot-com bubble burst and 9/11 didn’t add up to quite the same level of impact. (1970s OPEC-era stagflation wasn’t kind either, but inflation would have really eaten your money if you hid it under your mattress.) And no, I’m not going to start talking about hedging by buying gold instead in that sort of circumstance. We’ll come back to hedging against risks in some other article.

One of the dirty little secrets about stock picking, market timing, and the like: professional results are poor on average. Mutual fund managers, hedge funds, and tactical allocators show little persistent timing ability in most studies (e.g., Henriksson-Merton tests, DALBAR investor behavior reports). When they do show skill, it’s often concentrated in a tiny top percentile, not reliably replicable, and frequently offset by fees, taxes, trading costs, and behavioral mistakes. Everyone likes to drool over the Medallion Fund as an example of the canonically amazing hedge fund that always beats the market year after year for decades - and not just beats it but blows it away - but Renaissance Technologies also runs Renaissance Institutional Equities Fund (RIEF) and Renaissance Institutional Diversified Alpha (RIDA) and these do not consistently outperform the market or deliver the same extraordinary, market-crushing returns as their flagship, employee-only Medallion Fund. (And good lord, the fee structure on Medallion is equally legendary.) For instance, in 2020, the Medallion Fund famously surged 76%, RIEF lost 22.6% - and the S&P had a huge drawdown with the COVID crash but ended the year up 16% anyway.

Human psychology works against us - and it’s not like Wall Street is known for being well-adjusted mild-mannered overly rational sorts. Greed and fear rule the day; behavioral traps swing the markets… fear causes selling at bottoms; greed causes buying at tops. Overconfidence leads many to think they’re the exception, everyone knows a story of hubris…. yet Peter Lynch’s quip still holds: you don’t see famous market timers topping billionaire lists. (Though I think you could argue that Elon Musk is in some senses a market timer and a hype generator for his own meme stocks and freaking Dogecoin, but certainly that’s not what Lynch meant.)

There are rare cases where narrowly defined evidence-based tactical adjustments (e.g., some factor timing or using very specific signals in well understood conditions) show modest edges for sophisticated investors - but these are the exception, not something reliable for individuals or replicable en large. (That being said - you don’t have to have something that works everywhere in all environments to be highly successful - you just have to know where it works reliably and go be very successful there.) For almost everyone, the winning approach is:

Invest according to your goals, time horizon, and risk tolerance.

Diversify broadly (e.g., global stocks + bonds, and Buffett’s suggestion of an index fund is a solid place to start).

Stay invested through volatility.

Add regularly (dollar-cost averaging or other regular top-ups) rather than trying to guess tops/bottoms. It’s a popular aphorism that it’s good to have “dry powder” for when the market dips (meaning: cash, to invest when the market has bottomed out) - this is true, but it’s more true for illiquid markets like real estate.

Economist like to mythologize market efficiency to the point of unreasonableness but pretty much what it comes down to is that markets are efficient enough, and human psychology unreliable enough, that consistent market timing remains one of the most persistent (and expensive) myths in investing. If you’re tempted to try anyway, history suggests you’d be better off throwing darts than trusting your gut. (I say all that and I will come back later and talk about what I have seen work in particular circumstances. But unsurprisingly, it’ll probably one of the series of articles I’m planning to be behind the paywall. The very short version of that story: you can find things that work pretty reliably in certain circumstances, very little that works everywhere and broadly, but you don’t need a boil-the-ocean solution, you need to find your niche where you can make a fortune.)

So. Some operational and pragmatic advice, then.

If you are just getting started - or if you want to review and make sure you are proceeding from a stable footing, here’s the baseline recommendation I’d give to someone just coming into the market to invest. I hesitate to call this a beginner guide or anything more meme-tastic (despite my love for writing articles about internet memes, I feel like “noob guide to stock investing” is not going to go over tremendously well)

Get your financial foundation in place first

Build an emergency fund (3–6 months of expenses in a FDIC-insured savings account - or comparably secured at your credit union or in whatever jurisdiction you live if outside the US). Pay off high-interest debt (like your credit cards - basically anything over maybe 7%). Only invest money you can leave invested long-term. Basically, you don’t want to have to keep dipping into your investment portfolio for cash needs, and you don’t want to have to margin it (by which I mean borrow against the value of your portfolio) to do key things like buy a house or pay important bills.

Choose where to invest (which brokerage you are going to use)

Open an online brokerage account (probably). Popular beginner-friendly options in 2026 include Fidelity, Vanguard, Charles Schwab, eTrade, Robinhood (simpler interface, but fewer research tools), Webull or others with strong mobile apps. Your bank or credit union may offer an integrated platform also, and credit unions in particular tend to have a very inexpensive if clunky option - this is often fine at first, you may not need something glamorous - but the actual brokerage firms generally do it better. Do see if you can get something that lets you buy both for a conventional account and into your IRA, though. Most offer $0 commissions, fractional shares (buy $50 of Amazon instead of a full share), and easy app-based investing.

Decide what to buy

For most beginners, avoid picking individual stocks at first (it’s hard to beat the market consistently, and you can lose big on bad picks). Instead, focus on low-cost, diversified options. (Having said that: an important exception - you may be in the fortunate position to get equity ownership in a company because you work for them, from an ESPP - employee stock purchase plan - or stock options, Restricted Stock Units, or other forms of equity grant - in which case you should probably be quite interested in this and should as a rule want to glom on to this; these tend to be very advantageous terms as compared to general purpose investors. But do your homework, they can be difficult, especially if the stock is still private.)

The recommendation instead, as you probably recall from above, is to invest into index funds / ETFs - these track broad market indexes like the S&P 500. Popular choices will be VOO or SPY (tracks S&P 500), VTI (total U.S. stock market), VXUS (international stocks). These give instant diversification across hundreds/thousands of companies with very low fees (often less than 0.05% - yes, it’s gotten that efficient). A simple starter portfolio could be 80% U.S. stocks (e.g. by buying the VOO S&P 500 ETF) and 20% international stocks (the VXUS ETF) - then you could add bonds later for stability if you’re closer to needing the money. Or if you don’t want to deal with international markets, you could just buy SPY or VOO thereby getting exposure to the S&P 500 and start there.

Next step: invest regularly (people like to call this “dollar-cost averaging”)

Put in a fixed amount every month (e.g., $200–$500) regardless of market highs/lows. Whatever you can reasonably allocate. If you really want to be methodical about this, divide it out so that you’re putting a hundred bucks to work every Monday - or twenty bucks every trading day - some places will let you automate this, otherwise it will be insanely tedious. This reduces the risk of buying everything right before a drop and lets you buy more shares when prices are low. Some of this should ideally go into your retirement planning (which is usually your IRA or your 401k, and I’ll be back with an article about that sort of thing here shortly too.) Don’t put yourself in a tight spot, but consider this to basically be “long term savings” and something you don’t want to touch.

And conveniently enough, that leads me to my next point, which is: hold long-term.

The biggest mistake beginners make is panic-selling during downturns. Time in the market beats timing the market. Historically, staying invested through full cycles produces the best results. As you’ve learned in other activities, pulling out too early satisfies no one. (Did he just say that?)

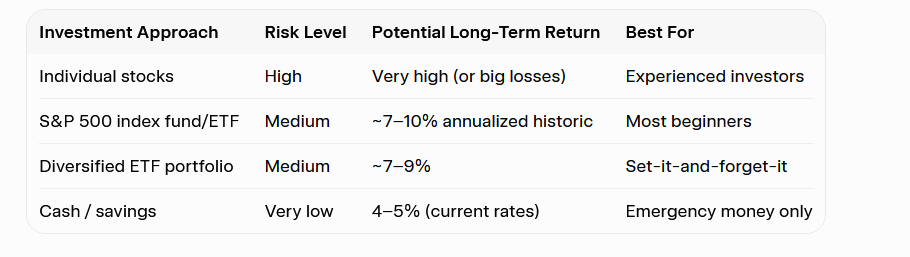

Quick Risk vs. Reward Summary

And yes, there are many more complicated things you can do - put and call options, collars or straddles, and various other speculative financial contracts that exist around the ecosystem of the stock market. Let’s not start there. If there’s interest, I can talk about some of that later as well, it’s been … dramatically impactful for me over the years, as some of you already know.

Final tips for investors just getting started:

Start small… even fifty or a hundred bucks a month compounds pretty well over decades, especially since you’ll likely be able to increase that in the years to come as your salary increases commensurately.

Educate yourself gradually (there’s good free resources like Khan Academy investing courses, Vanguard/Fidelity learning centers, there’s even some smart folks writing here on Substack heaven forbid!). It’s still worth reading the Wall Street Journal and Forbes, but they’re less critical than the days when print media ruled everything.

Ignore or at least minimize daily news noise and hot tips… focus on consistent, boring investing. Especially don’t take hot tips that are actually insider trading advice, this rather famously got SAC Capital Advisors / Steven Cohen in legendary levels of hot water back in 2013 (but he’s only the poster child for what’s been an endemic problem as long as you could get an “extra edge” out of illicit knowledge). Especially if you’re on an dollar-cost-averaged gradual investment plan that buys into an index fund - you’re really not going to trade the news, so don’t obsess about whatever twaddle gets blasted over social media hypebots.

Consider tax-advantaged accounts if available in your country (e.g., IRA/401(k) in the US, ISA in the UK). It’ll help you save for the long term - and there’s generally some advantageous rules about cases where you can at least temporarily borrow back out of them in a few key circumstances for things you might consider highly important like going back to school or buying a house.

Current Market Context (as of late February 2026)

The S&P 500 is hovering around 6,800 after some recent volatility, particularly in tech/AI names like Nvidia (which saw big swings post-earnings). Wall Street analysts generally expect positive returns for 2026 overall (~10–12% consensus in some forecasts), driven by continued earnings growth, though with higher volatility possible due to inflation readings, AI hype cycles cooling in spots, and sector rotation (away from pure tech toward value/industrials in some views). Broader economic growth looks resilient, but nothing is guaranteed - markets can correct or pull back at any time and the political scene makes things more volatile than most; as I write this, there appears to be another attack underway with Israeli and US forces bombing Iran which I’m sure will cause market consternation.

I hope you have found this a useful introduction to the topic. I will be back with a number of other articles on various financial topics that may be of interest to many of you - I expect my next one will cover some level of general purpose things to look at for your taxes, since we’re on the edge of tax season for the United States. After that, I’m expecting to do a series of articles where I go into some more esoteric topics that might save you a lot more money if you happen to be in certain high net worth situations, based on my hedge fund and entrepreneurship experiences, and those I am planning to finally introduce a paywalled section (more for the prospect of getting Substack social credit and the proverbial orange checkmark rather than the thought of making a vast fortune from my writing here, as you may have surmised). But we shall leave that for another day. Feel free to comment or message me with requests for topics if there’s anything you’d like me to cover in future articles; I have a litany of areas upon which I intend to write but I do intend to take audience requests into account.

I look forward to the next installment.

I do like pieces on investing and I’ve been in the game since an old Indonesian friend I met on my first job at a grocery store got me into it and worked as an accountant full time. Then only did the side hustle as at the grocery store for extra cash like a true Chindo king.