Tax Season Approaches: Are You Prepared?

Everyone's least favorite time of year

Someday, we will all be lying on our backs

Free at last from income tax

- You Picked A Real Bad Time, Billy Joel

Paying taxes is… not the sort of thing that fills anyone with joy. (I can think of exactly one person who always claimed otherwise - Gary was fond of saying “Well, it meant I made money that year” and I suppose I can't particularly argue with that - but I wager he still itemized his tax deductions.) But it’s generally a reasonable idea to retain (or at least direct) as much of your money as is legally permitted, because I think in general there’s a fairly common belief that the government is probably going to spend a decent sized chunk of your taxes on things you would really rather not want to personally support. (Depending on what your beliefs are, of course, this varies dramatically: some people may say “I would be happy to fund education for everyone and I don’t want it spent blowing up poor SOBs in some banana republic part of the world” - others may think that our education system has turned into woke brainwashing and exists to export Hollywood cultural hegemony, and would much rather focus on health care, life skills, jobs, and security for American citizens with particular emphasis on veterans and young Americans. I’m not here to advocate for any particular model at this point - hell, both of those perspectives might be right - I’m here to talk about financial strategies.)

There are a lot of things people commonly do to reduce their tax burden; here are some good choices applicable to many people. This particular piece is all terribly dry and I haven’t hidden any interesting stories herein, so if you read my writings for my snarky observations or my industry stories - this isn’t that sort of piece, this is just about saving you money. And while I’m intending to follow on this piece with a number of Substack articles that might be (at least partially) paywalled and focused on esoteric ways that might save you more money, especially for folks with higher earnings - consider this to be the general introduction to the topic, applicable to most middle-income (and higher) Americans and a good general checklist.

Or to put it another way - this advice I’ll give you for free, and you’re more than welcome to go to a better tax guy than me if this is the tier of tax advice that best suits you. The sorts of things that I’m likely to follow on with later are perhaps a little more esoteric - like, how to structure your charitable giving for tax benefit; how to invest in art for economic gain (for most of us, this is dubious) or at least for tax mitigation purposes (this is far more doable); how to move money out of China or India or other jurisdictions with capital controls; that sort of thing… and while you may not, strictly speaking, be in the market for this, I figure you may be aspirationally in the market for it (if things go well for you) or just interested in hearing stories of how thing are or were done in the hedge fund world (as well as what you weren’t allowed to do, and perhaps some pointed examples of people who got busted for stepping over the lines…) But let’s come back to that, shall we? For the moment, let’s focus on how to save you some money in the near term.

There are many legitimate, and even (heaven forbid) IRS-approved ways to reduce your federal income tax burden in 2026 (for income earned this year, reported on your 2026 tax return filed in 2027) - most of these are applicable to your 2025 taxes but it’s a little late to take advantage of most of them. These strategies focus on lowering taxable income, claiming deductions/credits, deferring income, or shifting to tax-advantaged accounts. Effectiveness depends on your filing status, income level, employment type (e.g., W-2 vs. self-employed), age, state, and whether you itemize or take the standard deduction. Spoilers: you should generally itemize, if you can, especially if you own your own house or have non-trivial stock transactions - or big expenses in certain categories. If you rent or otherwise are just getting started though, it may not be really all that worthwhile. So I’m going to give you some recommendations based on a couple different income brackets.

And for simplicity’s sake, we’re going to call these Renters and Owners, because this is usually what’s going to make the distinction for you. But really, it’s probably more what I mean here is something like Lower Earners and Higher Earners, and this is still mostly a middle-class split. If you’re living at the poverty line, you’re probably not paying a lot of tax anyway (hopefully, you’re actually benefiting from various aid programs) and probably not able to get a lot of advantage from this advice, other than learning for the future if you happen to be, for instance, an impoverished grad student.

The huge omnibus One Big Beautiful Bill Act of 2025 (I still can’t believe they called it that - we’ll abbreviate it here as the BBB) made many 2017 TCJA (Tax Cuts and Jobs Act) provisions permanent (e.g., individual tax brackets and rates, higher standard deduction), increased some caps (like State and Local Taxes - which gets abbreviated here as SALT), and added new deductions/credits. Tax brackets remain progressive, starting off at 10% and graduating up to the top rate at 37%, so for instance:

Tax brackets (simplified for single filers; double thresholds roughly for joint):

10%: $0 – $12,400

12%: $12,401 – $50,400

22%: $50,401 – $105,700

And so on up to 37% over ~$640,600.

Anyway, here’s my extremely broad recommendation. Reading about taxes is not exciting (writing about taxes doesn’t really knock my socks off either, and the fun stuff - as it were - is going to come later anyway, when we talk about things that you can do if you’re in some very special situations). You’re more than welcome to read the whole thing and look for where I’m snarky, that seems to always be what my readers/students enjoy; I try to be more straightforward/practical herein and less snarky than usual. But this is basically split into two income bands, both basically targeting middle class and professional Americans in various stages of life; if you’re sufficiently upper class income you may need further assistance and you likely know that (hell, you may need a family office) and below a certain level of income you’re just not going to get much help from any set of tax recommendations and would be better served by recommendations for what programs can help you (which generally are not based on your tax refund).

So I’m going to start with the group I’m calling Renters - but keep in mind this basically means folks earning a middle class wage but generally not yet a homeowner or significant investor, so the primary differentiator for a tax purpose is whether it’s worth itemizing your deductions. Here are some practical, legal ways for the average person (middle-class wage earner, not ultra-high-income) to reduce their federal tax burden in the current environment (2026 tax year). These focus on common, accessible strategies that don’t require complex setups like businesses or massive investments. Many involve lowering taxable income through deductions, pre-tax contributions, or credits.

Obligatory disclaimer: tax laws can change, you probably have state or local tax laws to deal with too, and your situation (filing status, marital status, what state you live in especially if it changes during the year, income level and any windfalls you like inheritance) matters, so consider consulting a tax professional or using reliable software for personalized advice. But this much is free - so give a read, take some notes, and see where you can make an impact first.

Start by maximizing your pre-tax retirement contributions. Contributing to retirement accounts reduces your taxable income directly (for traditional accounts). Usually this will be your IRA and your 401(k) (if your employer offers it). The Roth IRA is more advantageous if you’re a higher earner - taking the tax hit now so that you don’t take it during retirement - but currently your tax bracket is probably relatively modest so don’t want to do that, so what you’ll want is called the Traditional IRA - to which you can contribute up to $7,500 (plus $1,100 catch-up if 50+). It’s deductible if you meet income limits (which get phased out at higher incomes if covered by a workplace plan). As far as the 401(k), (and also the 403(b), or similar employer plans) - you can contribute up to $24,500 in 2026 (plus an $8,000 catch-up if age 50+). These are pre-tax, so they lower your adjusted gross income (AGI) immediately. If your employer matches, that’s free money too. You don’t get to use it right away, but as far as saving for retirement - really hard to beat. And there’s ways to borrow against it for key expenses in the future, if you need to, though really - try not to.

These are among the most powerful and straightforward moves for salaried workers.

Use Health Savings Accounts (HSAs) if you’re eligible. If you have a high-deductible health plan (HDHP), contributions are pre-tax (or deductible), growth is tax-free, and qualified medical withdrawals are tax-free. 2026 limits are typically around $4,300–$4,500 individual / $8,500–$9,000 family (exact figures adjust annually; check IRS updates). This triples the tax advantage compared to regular savings. Even if you don’t need the money now, you can save receipts and reimburse yourself later.

This next one is going to sound stupidly obvious, but: claim all your eligible deductions and credits. Take what’s available to lower taxable income or taxes owed dollar-for-dollar (credits are better).

The standard deduction - which is what most people take instead of itemizing - for 2026: $16,100 (single), $32,200 (married filing jointly), $24,150 (head of household). It’s often higher than itemized for average filers. Thanks to some recent generosity in the Big Beautiful Bill and related legislation, there’s an additional benefit for seniors: If you’re 65+, you can take an extra $6,000 deduction (through 2028 under recent changes). At the other end of the spectrum there’s Child Tax Credit, Earned Income Tax Credit (EITC), education credits, or energy credits - if you qualify (e.g., dependents, low-to-moderate income), these directly reduce taxes owed. And to whatever extent you can manage, charitable contributions - currently there’s new above-the-line deduction up to $1,000 ($2,000 joint) even if you take the standard deduction.

Other practical strategies for most people - though this requires you to prepare now rather than at the last moment (like you might currently be doing, cough) - adjust your W-4 withholding, by which I mean insure accurate withholding to avoid overpaying (we all hate making an interest-free loan to the government) or underpaying (we all even more hate paying penalties for not withholding enough taxes). Update it via your payroll department if you had big changes. If you have investments: Consider tax-loss harvesting, which is a fancy term for “sell losing investments to offset gains” (up to $3,000 against ordinary income). If applicable, make use of Flexible Spending Accounts (FSAs) or Dependent Care - use pre-tax dollars for medical or childcare expenses if offered by your employer. If in a high-tax state - for instance: California, New York, Hawaii, New Jersey: Check the increased SALT deduction cap (now $40,000+ under recent laws), though most average filers stick with the standard deduction.

Start early in the year for contributions and planning… the earlier you act (e.g., increasing 401(k) withholding), the more compound benefit you get. For many middle-income households, maxing retirement accounts and claiming credits/deductions can cut the effective tax rate noticeably without exotic moves. Since you’re currently agonizing over your taxes, you might as well make these changes now, it will make next year less painful.

(My advice if you’re in the low-income bracket, maybe even below the typical renter tier and more in the part time work study student tier, and can’t afford to put away money for any of these other things: take whatever deductions you can. If your health care plan is lousy - most are - do something with your health saving account; if your job offers a decent 401k especially with matching, see if you can squirrel away a few bucks in it. But if you’re just in the part-time-income bracket, you may get everything back anyway from just your baseline standard deduction and any other deductions you may easily qualify for. If you’re still young, piggyback on your parents health care plan if you can get away with it - or the school plan if you’re in university - it will tend to be better than trying to get by on the heartburn-tier plans available with entry jobs.)

OK, let’s say you make a higher income bracket, or you own your house, or you have investments - I’ve split this article as mentioned above and this next section is targeted at the category of higher earners that I previously referred to as Owners. Keep in mind that this basically means people who benefit from itemizing their deductions - generally because they own property; it doesn’t always line up that way but it frequently does. This next section is intended for you.

A lot of this mirrors the above. The proven ways to reduce your tax burden are fairly consistent. Here are some of the most effective and commonly recommended strategies for 2026:

Maximize your contributions to tax-deferred retirement accounts. Contribute pre-tax dollars to lower your current taxable income. Your biggest bang for the buck is 401(k), 403(b), or similar employer plans which let you get up to $24,500 (under 50), $32,500 (50+), or $35,750 (ages 60–63 with enhanced catch-up under recent rules). Employer matches - if your firm does them - are just gravy on top, they basically just add free money. But all the more reason to max this out if you can. If you can’t get those, a SIMPLE IRA is a good employer choice, and I’ll talk about that below - but a 401(k) is generally better.

Next is the Traditional IRA: up to $7,500 (under 50) or $8,600 (50+); deductibility phases out at higher incomes if covered by a workplace plan. Now, many folks are going to want to use a Roth IRA - because basically you pay the taxes now so that you aren’t taxed on it when you withdraw it in retirement - but there’s a particularly useful way to do this, which is termed the “backdoor conversion” (or “mega backdoor”) - basically, contribute after-tax to a traditional IRA (backdoor) or 401(k) after-tax (mega), then convert to Roth for tax-free growth. No income limits on conversions, but watch pro-rata rule for backdoor.

There’s also various self-employed options (e.g., SEP-IRA, Solo 401(k)): Much higher limits (up to 25% of net self-employment income or more). This is definitely worth looking into if you qualify - although of course you’re unlikely to get the benefit of employer matching!

I will reiterate my earlier recommendation to use a Health Savings Account (HSA) when feasible - it effectively gives triple tax advantage: pre-tax contributions, tax-free growth, tax-free withdrawals for qualified medical expenses. The 2026 limits: $4,300 (individual) or $8,550 (family), plus $1,000 catch-up if 55+. Requires a high-deductible health plan (HDHP). Bronze/catastrophic plans may now qualify under the BBB changes - I am not 100% sure of that, but this is my understanding (the Big Beautiful Bill did poke a stick at Obamacare/the Affordable Care Act but as of my most recent understanding this part may work in your favor).

Of course you should take care to claim all the deductions and credits that are coming to you. This will be more work than the Renter class - because you almost assuredly need to itemize everything. Mortgage interest (up to $750k debt limit for post-2017 loans), property taxes, charitable donations (new above-the-line cash donation deduction of $1,000 single/$2,000 joint even if not itemizing). If somehow that doesn’t add up to more than your standard deduction, you can still take your standard deduction. Also, the SALT (State And Local Tax) cap is increased to $40,000 under the BBB (with phaseouts/inflation adjustments) - so if you’re stuck in a high tax state, you might as well get back what you can. Consider pass-through entity (PTE) elections if you are self-employed or a business owner. Also common deductions for many folks: student loan interest, educator expenses, energy-efficient home improvements (some credits persist or have changed).

One of the more relevant means for homeowners is mortgage interest deductions. Mortgage interest is still tax-deductible in 2026, but only if you itemize deductions on your federal tax return (Schedule A of Form 1040). It’s not available if you take the standard deduction. This deduction applies to qualified home mortgage interest paid on loans secured by your main home or a second home. Key rules remain in effect under current IRS guidelines (including Publication 936 for 2025 returns, which carry forward similarly for 2026 unless updated).

You can generally deduct interest on up to $750,000 of qualified home acquisition debt ($375,000 if married filing separately). This applies to loans taken out after December 15, 2017, to buy, build, or substantially improve the home. If the debt was incurred on or before December 15, 2017 (or under a binding contract closed before April 1, 2018), you can deduct interest on up to $1 million ($500,000 if married filing separately), plus any grandfathered debt. Now, home equity loans (and HELOCs) are treated slightly differently: Interest is not deductible unless the proceeds are used to buy, build, or substantially improve the home securing the loan (i.e., treated as acquisition debt). This restriction (from the 2017 TCJA) remains in place. This means don’t be an idiot and refi your house so that you can take out a bunch of money and buy yourself a boat.

To deduct mortage interest, the loan must be secured by a qualified home (your main or second residence), you must have ownership interest, and both parties must intend repayment (this does, occasionally, actually come up). Points may also be deductible under certain rules. Mortgage insurance premiums (PMI) are no longer deductible in most cases (expired previously).

If you’ve got investments, you probably didn’t have a perfect track record - which means you may be able to do what’s politely referred to as Tax-Loss Harvesting. Sell investments at a loss to offset capital gains (unlimited) or up to $3,000 of ordinary income. Carry forward excess losses. Do this before year-end. I have friends who are still carrying forward losses from the dot-com days - $3,000 a year only goes so far.

I’m going to come back with another article or three later on and talk more about charitable giving - but for now, just take it as a to-do: Donate cash, appreciated stock (which lets you avoid capital gains tax), or bunch donations into one year to exceed standard deduction and itemize.

To the extent that it’s under your control - and I realize it isn’t always, but a little clever negotiation can often bear fruit, it’s worth considering timing income and expenses as a tax planning strategy. Defer bonuses/income to 2027 if in a high bracket now. Accelerate deductible expenses (e.g., prepay property taxes, make January charitable gifts in December). For the self-employed: Deduct business expenses, home office, QBI (20% deduction on qualified business income… still available).

Then there’s some other … specialized strategies. I’m just going to mention them, and leave you to look into them if they’re applicable to you. Or if a bunch of people ask about any one, I can write further about it. There’s 529 plans for saving for education: contributions may get state tax breaks; and growth tax-free for qualified use. Investment made in Opportunity Zones/QOFs can be given particularly preferential treatment: this deserves a great deal of description but approximately you defer capital gains taxes by reinvesting (and sometimes you get some particularly sweetheart terms or get outrageous treatment for foreign investors or the like). Roth conversions can be used to convert traditional IRA/401(k) funds in low-income years to fill lower brackets and reduce future Required Minimum Distribution (RMD) taxes. There are also some new provisions under the BBB that I’m informed of but not really familiar with: some senior-specific deductions, potential car loan interest deductions for U.S.-assembled vehicles, and various other targeted breaks. Qualified Small Business Stock (QSBS) can be rolled over into other startup investments; a real estate 1031 election also lets you defer gains by rolling them over into a new property. Sometimes state law will work against you on this front even if federal law supports it - there’s some ridiculously entrepreneur unfriendly things happening in California and Washington at the moment - but be aware of what that looks like, too.

As general advice, you want to try to plan year-round (and stay ahead of this) because you may need to adjust withholding/estimated payments to avoid underpayment penalties (fines) or large refunds (which are interest-free loans to the IRS). Investment income from stock trades and the like, or sizable bonuses, tends to throw off your calculations as compared to relatively smooth salary income. For those who are high earners or self-employed and can afford to sock it away, focus on retirement maximization, Qualified Business Income (QBI), Pass-Through-Entities (PTE) for SALT, and business structuring (e.g., S-corp or S-corp election for LLCs to reduce self-employment taxes). And of course, run the numbers - use tax software or a spreadsheet to model scenarios - it always pays to doublecheck, for instance, does itemizing beat the standard deduction?

Of course, obligatory disclaimer: These are general strategies based on current 2026 IRS rules and recent legislation (e.g., BBB extensions). Tax laws are complex, and your situation (e.g., income phaseouts, state taxes) matters. Always consult a tax professional, CPA, or financial advisor for personalized advice, proper reporting (e.g., Form 8606 for conversions), and to avoid audits or penalties. Check irs.gov for the latest publications like 590-A/B (IRAs) or 936 (home mortgage interest).

OK so after all that! Is your head spinning like the proverbial cartoon character yet?

It might be a little helpful for some people to look at a couple of common bugaboos in this process.

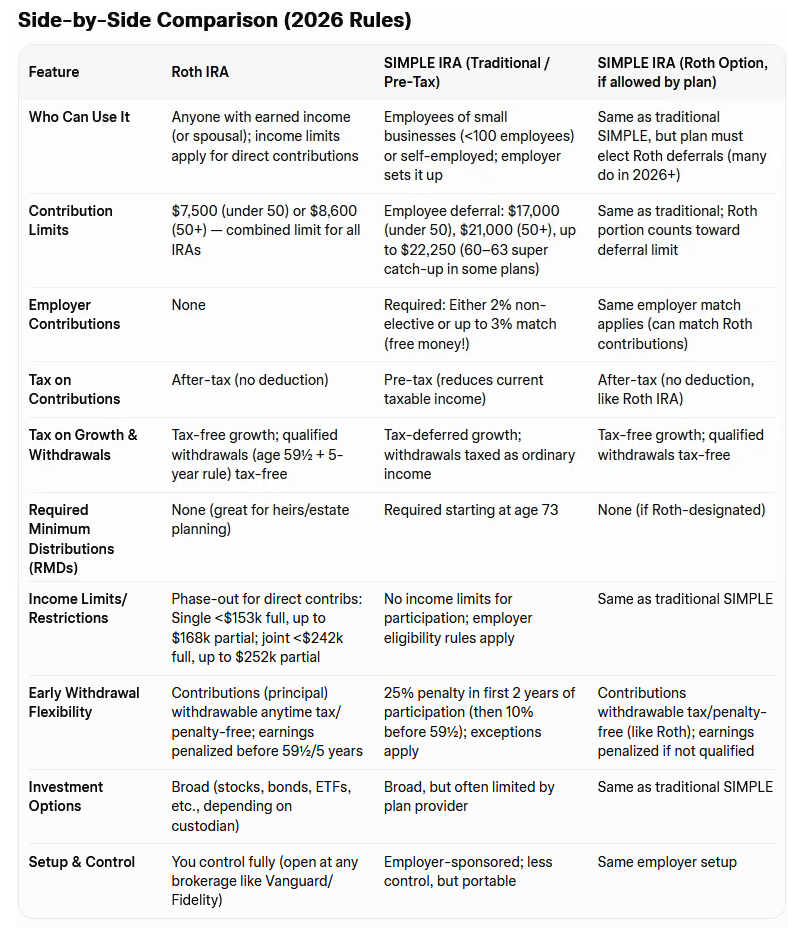

Different types of IRAs: Traditional IRAs, Roth IRAs, and SIMPLE IRAs (which are not in fact simple, it’s an acronym). Why would you choose one over another? What really is an IRA? The days when I could make jokes about the Irish Republican Army have come and gone, everyone just stares at me blankly unless I’m in Boston. An Individual Retirement Account is a means by which you can save money for retirement on a tax advantaged basis, and to vastly oversimplify: when they first came up with it, you could basically put money into an IRA from your paycheck before tax and it wouldn’t be taxed until you withdrew it when you retired. Since you presumably wouldn't otherwise be earning at that point, you would be in a lower income bracket, and would pay a lower tax rate at that point. On the other hand, if you thought you were going to keep working for quite a while and have to start taking mandatory disbursements (RMDs - Required Minimum Distributions) while you were still drawing a paycheck, you might end up with quite a tax bill, or you might have a good income from other dividends or sources by that point - so in that case, it might be advantageous for you to pay your taxes now so that you could withdraw money at retirement time having already paid your taxes on it - and that’s the premise behind a Roth IRA. So that split is hopefully fairly straightforward to understand, it’s just whether you’re taxed when the money goes into the savings account or when it comes out.

For people who are asking “Why am I worrying about what my tax rate is going to be when I’m retired? I don’t expect to be getting anything but social security then and heaven knows it’s dubious if social security will even be solvent by that point?” - do keep in mind that it has historically been at least somewhat common for people to draw a pension upon retirement. This is, of course, less common these days in the United States. But the thought that you might have an annuity, a pension, dividends, or some sort of income even once you retire is not unfathomable. Even the proverbial part time job or Etsy store or the like is a potential source of income. But this, fundamentally, is why you might choose a Roth IRA over a Traditional IRA - or perhaps, why you wouldn’t.

And then amusingly/ironically, to complicate things, there’s SIMPLE IRAs: (Savings Incentive Match Plan for Employees) which is an employer-sponsored plan (similar to the structure of a 401(k)) for small businesses or self-employed individuals, traditionally with pre-tax contributions. SIMPLE IRAs have traditionally been Traditional IRAs only (pun intended) but that has just changed.

Many SIMPLE IRA plans now allow Roth-designated contributions (after-tax, like a Roth) thanks to SECURE 2.0 Act changes starting in 2026. This is probably clear as mud. Try this chart for clarity.

Why would you opt for a Roth IRA? Well, the most important reason is tax-free retirement income - this is ideal if you expect to be in a higher tax bracket in retirement (e.g., due to rising rates, large savings, or other income like pensions/Social Security). Simultaneously, no RMDs - You can let your money grow indefinitely or pass it tax-free to heirs. It gives you flexibility - you can withdraw contributions anytime without penalty/tax (consider this to be basically “emergency access”). And as compared to the SIMPLE IRA, it gives you independence - there’s no employer needed; this makes it great as a supplement or for self-employed/high earners (and as always, use a backdoor Roth if your base income is too high). It’s the best choice if you’re in a lower current tax bracket, want tax diversification, or prioritize estate planning.

Conversely, why might you choose a SIMPLE IRA, especially a traditional one?

Total contribution size is a bit one - the combination of higher contribution limits and employer match - up to $17k–$22k, plus employee deferral, also plus the “free money” aspect of mandatory employer contribution (2–3% of pay) … which often equates to more savings power than a Roth IRA alone. In addition, it gives you an immediate tax break - since pre-tax contributions lower your current taxable income (this can be valuable if you happen to be in a high bracket now). It’s simpler for small businesses - it’s an easier/cheaper setup than a 401(k); good for self-employed or small firms. In general, best choice if you expect a lower tax bracket in retirement, want to maximize savings with employer help, or need the upfront deduction.

Or of course, there’s the option to use both. Many people do and if you have the option to do so - and the spare income to allocate to take advantage of it - it’s a very solid choice. If you are eligible for a SIMPLE IRA through work/self-employment, max it (especially for the employer match - anytime you can get free money, rake it in), then add a Roth IRA for tax-free growth on additional savings. This creates a mix: pre-tax (SIMPLE) + after-tax (Roth) for flexibility in retirement withdrawals.

The choice is a pretty straightforward split, and a possible best-of both worlds option. Prefer the Roth IRA if the tax-free withdrawals, no RMDs, and flexibility matter more than maxing contributions or getting an upfront deduction. Prefer the SIMPLE IRA if the higher limits, employer contributions, and current tax savings are priorities (especially traditional pre-tax version). With Roth options in SIMPLE plans now available, consider Roth-designated contributions in your SIMPLE for the best of both worlds (higher limits + tax-free growth).

And of course, once again as boilerplate disclaimer: your choice hinges on your current vs. future tax situation, income, and whether you have access to an employer plan. Rules are based on 2026 IRS guidelines (e.g., Notice 2025-67). Consult a tax advisor or financial planner to model your scenario—factors like state taxes, overall portfolio, and retirement timeline make a big difference. Check irs.gov for the latest on retirement plans.

Why did I say earlier that the 401(k) is better? Ahh, you’re observant. Kudos to the ones who pay attention. The answer is multifaceted, but basically the key points are: contribution limits are better (higher) than the SIMPLE IRA, the Roth Mega Backdoor is generally equally or more effective (if you choose to do it - you don’t need to), and employer matching can be larger for a 401(k) and its ilk (it isn’t guaranteed to be, though, so do compare if you have the option of both).

So speaking of the Roth backdoor conversion, which sounds like it ought to the sort of thing not mentioned in polite company, let’s shed a little light on that topic.

The backdoor Roth IRA is a popular, legal strategy that allows high-income earners to contribute to a Roth IRA even if their income exceeds the IRS limits for direct Roth contributions. It’s not a special account type, it’s a two-step process using a traditional IRA as an intermediary. On my more exasperated days I’d say it’s just an exercise in bureaucracy and paper shuffling, but what the hell, it can save you a lot of money, so roll your eyes/hold your nose and do the dance, I guess. Just make sure you follow all the steps and leave yourself enough time to do it.

I’ve sort of covered this earlier but as a recap as to why you’d want to use this: Roth IRAs offer some key advantages… contributions are made with after-tax dollars, growth is tax-free, and qualified withdrawals in retirement (after age 59½ and a 5-year holding period) are entirely tax-free. However, direct contributions to a Roth IRA are phased out or eliminated at higher income levels.

For tax year 2026 (current as of the end of February 2026) the annual IRA contribution limit (applicable to both traditional and Roth IRAs combined) is $7,500 (or $8,600 if age 50 or older).

Roth IRA direct contribution phase-out ranges (based on modified adjusted gross income, or MAGI):

Single / head of household: Full contribution if MAGI < $153,000; partial between $153,000–$168,000; $0 if ≥ $168,000.

Married filing jointly: Full if MAGI < $242,000; partial between $242,000–$252,000; $0 if ≥ $252,000.

Married filing separately (living with spouse): Very limited, usually $0.

If you’re above these thresholds (common for many professionals), you can’t contribute directly to a Roth IRA - but the backdoor strategy lets you effectively do so.

Here’s your step-by-step process for how the backdoor Roth process works - it’s not actually that complicated, it’s just a bit of a paperwork shuffle.

First, you contribute to a Traditional IRA (the nondeductible variety.) Open (or use) a traditional IRA and make a nondeductible contribution (after-tax dollars - no upfront tax deduction). Contribute up to the annual limit ($7,500 or $8,600 in 2026). This step bypasses Roth income limits because traditional IRA contributions have no income restriction (though deductibility does for high earners).

Second, you file to convert to a Roth IRA. Shortly after (often immediately or within days/weeks to minimize any growth and potential taxes), convert the contributed amount from the traditional IRA to a Roth IRA. Conversions have no income limits. Since the contribution was nondeductible (after-tax), the conversion is generally tax-free on the principal amount (you already paid taxes on it). Any earnings between contribution and conversion are taxable, so this can sometimes be a little bit of a challenge, but is generally relatively minimal. Usually, most places that will domicile your IRA will be used to doing Roth conversions - eg Vanguard or the like - but it helps to pick someplace familiar with the process. At least check the website (or talk with the customer service agent/banker/etc) to make sure that this isn’t going to be an enormous pain in the butt when it comes time to do this.

Then, report it properly. File IRS Form 8606 with your tax return for the year of the nondeductible contribution to track your after-tax basis. This prevents double taxation later. You’ll also report the conversion on your taxes.

Here’s an important caveat emptor: the pro-rata rule. This is the biggest potential pitfall. The IRS treats all your traditional, SEP, and SIMPLE IRAs as one big account for conversion purposes. If you have pre-tax money (e.g., deductible contributions, rollovers from old 401(k)s, or earnings) in any traditional IRA, the conversion is pro-rated between pre-tax and after-tax amounts. Example: You have $50,000 in pre-tax traditional IRA assets + $7,500 nondeductible backdoor contribution (total $57,500). Converting $7,500 would be about 87% pre-tax (taxable) and 13% after-tax (nontaxable) - you’d owe taxes on most of it. To avoid this and make the backdoor clean/tax-free… ideally, have no pre-tax traditional IRA balances (or very minimal). But if you can’t do that, a common fix is to roll your pre-tax IRA funds into an employer plan like a 401(k) first (if allowed), then do the backdoor.

Is this sort of thing going to be the right choice for you? Probably, if high income blocks direct Roth contributions, you want tax-free growth/withdrawals, and you can keep traditional IRAs empty of pre-tax funds. Roth has some solid advantages: No required minimum distributions (RMDs) in Roth IRAs (unlike traditional), and it’s great for estate planning (heirs inherit tax-free). It’s not helpful if you expect to be in a much lower tax bracket in retirement (traditional might be better). Some debate exists on long-term IRS views, but it’s widely accepted and used (endorsed by major firms like Vanguard, Fidelity, Schwab) so it’s not likely to change course anytime swiftly

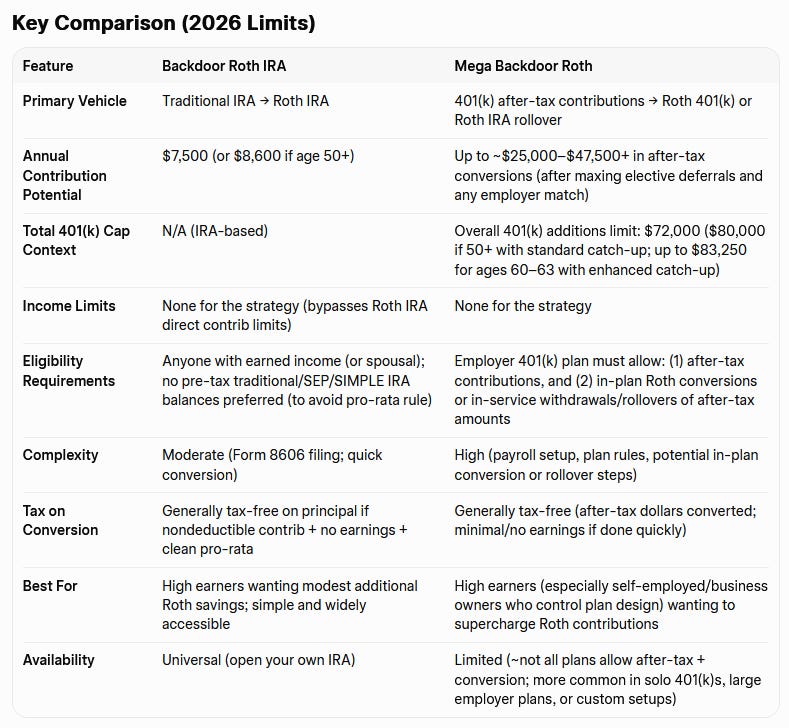

The backdoor Roth IRA and mega backdoor Roth are both legal strategies that help high-income earners (who exceed Roth IRA direct contribution income limits) build tax-free retirement savings in Roth accounts. They achieve similar goals - getting after-tax dollars into a Roth for tax-free growth and qualified withdrawals - but differ significantly in scale, requirements, complexity, and accessibility.

Both remain fully available and unchanged in 2026 (no elimination under recent legislation like SECURE 2.0 or related updates).

How Each Works (Quick Recap)

Backdoor Roth IRA

Make a nondeductible (after-tax) contribution to a traditional IRA (up to $7,500/$8,600).

Convert to Roth IRA soon after (tax-free if no pre-tax IRA balances trigger pro-rata).

Pro-rata rule is the main hurdle: If you have existing pre-tax IRA money, part of the conversion becomes taxable.

Mega Backdoor Roth

Max your regular 401(k) deferrals (pre-tax or Roth): $24,500 (or $32,500 if 50+).

Contribute additional after-tax dollars via payroll (up to the overall $72,000+ cap, minus deferrals/match).

Convert/roll the after-tax portion (plus any minimal earnings) to a Roth 401(k) (in-plan) or Roth IRA (rollover).

Often automated in supportive plans; the “mega” comes from the much larger dollar amount possible.

Advantages & Disadvantages

Backdoor Roth IRA

Pros: Easy to set up (no employer plan needed); no RMDs in Roth IRA; flexible investments.

Cons: Low limit; pro-rata rule can create taxes if you have other IRAs (fix by rolling pre-tax to 401(k) first); only modest annual boost.

Mega Backdoor Roth

Pros: Dramatically higher contributions (5–6x more than backdoor); tax-free growth on large sums; can pair with employer match; great for aggressive savers/business owners.

Cons: Requires specific 401(k) features (many plans don’t offer after-tax or in-plan conversions); more administrative hassle; potential plan fees or restrictions; tied to employment/plan rules.

And inevitably, the question arises: which one should you use? My general recommendation would be to start with the backdoor Roth IRA if you’re above Roth income limits (~$153k–$168k single / $242k–$252k joint in 2026) and want a straightforward way to get $7,500+ into Roth annually - it’s accessible to almost everyone. Then, add or prioritize the mega backdoor Roth if your 401(k) (or solo 401(k) if self-employed) supports it and you’re maxing other savings - you can potentially add tens of thousands more to Roth each year for bigger long-term tax-free growth. Many people do both in the same year for maximum Roth accumulation. But you have to have a lot of spare savings that you can put aside to really take advantage of both! (More power to you, if so.)

Once again, the disclaimer - applicable to this section as well as the others. These strategies involve tax nuances (e.g., basis tracking, timing to avoid earnings taxes, state rules). Consult a tax advisor or financial planner to confirm your plan allows it, run pro-rata calculations, and ensure proper reporting (Form 8606 for backdoor; 1099-R for conversions). Rules are current as of 2026 per IRS guidelines.

I hope this has proven useful to you, and likewise has given you some ideas of how to save your bank account from some of the anguish it usually suffers this time every year. Plan out your financial road map with an eye towards how to make use of some of this advice, and may the year to come bring you peace, happiness, and prosperity.